What is the Accounts Receivable Turnover Ratio?

What is the Accounts Receivable Turnover Ratio?

Definition: The accounts receivable turnover ratio is an accounting measure that quantifies how effective a company is, at collecting receivables from clients. This ratio tells stakeholders how quickly a business can convert credit extended to customers into cash. Also known as debtor’s turnover ratio, the accounting metric displays the businesses’ efficiency when it comes to using assets.

Important to note, businesses use the net credit sales to compute the receivable turnover ratio. If the gross credit sales are used, the business is likely to come up with a wrong result. This is because unadjusted total credit sales lead to inflated readings.

Typically, the receivable turnover ratio enables businesses to keep track of their performance over the years. For example, the ratio for the just ended financial year may be compared to the previous year to gauge where the business stands in terms of revenue collection efficiency. Also, this ratio informs a business of where it stands relative to competitors in the industry.

Accounts Receivable Turnover Ratio Formula

The two main components used in computing accounts receivable ratio are net credit sales for the period in consideration. If the period under consideration is one financial year, then the accountant will put together the net sales for which the customers have not paid in yet during that year. On the other hand, there is the average of accounts receivable for the period in consideration. To this end, one computes the sum of the beginning accounts receivable and the ending accounts receivable and then divide by two.

Accounts Receivable Turnover Ratio Example

Let us see how this formula works in an example.

John, a junior accountant at a food company, has been requested by his seniors to compute the accounts receivable turnover ratio for year just ended. In addition, John is supposed to submit his assessment of the company’s efficiency in terms of revenue collection during this period in comparison to the past year.

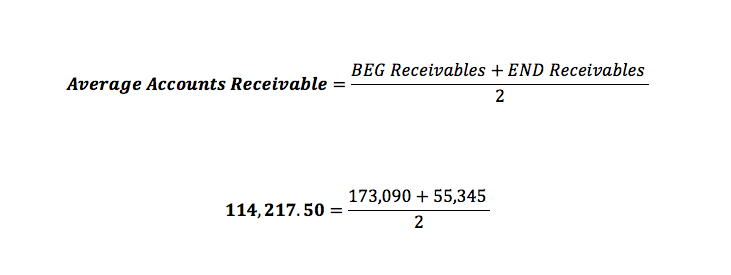

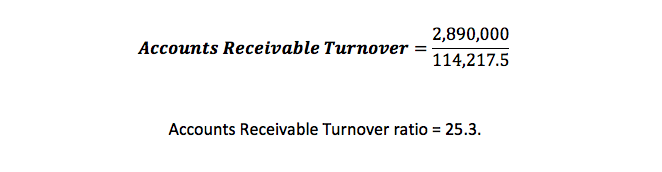

In the opening balance sheet for the year just ended, the company’s accounts receivable balance $55,345. The ending balance was up to $173,090. For the same period, the net credit sales amounted to $2,890,000. Using this information, John will calculate the accounts receivable turnover ratio as follows:

Step 1: Find the average accounts receivable for the year just ended.

Step 2: Compute the ratio

Accounts Receivable Turnover ratio = 25.3.

After computing the ratio, John needs to submit his assessment on whether the company’s performance in terms of revenue collection efficiency was better during the year just ended or not. According to the data available to John, the accounts receivable turnover for the previous year was 15. Compared to the year just ended, this ratio is smaller. What does this mean?

While in college, John learnt that a high accounts receivable turnover ratio implies that a company is efficient in terms of converting credit sales to cash. On the contrary, a lower account receivable turnover ratio indicates that the business is has poor credit policies. Also, this could be evidence that the business’ customers are not creditworthy. Looking at the two ratios, it is evident to John that the business was more efficient in collecting revenue during the year just ended compared to the past year. This is the assessment that he submits to his seniors.

Summary

Businesses have various efficiency ratios that they track to ensure they are operating at or near optimum potential. In particular, tracking the accounts receivable turnover ratio ensures that the business remains viable. The trend of the ratio over time informs stakeholders concerning the financial health of the business.

Contents